Good morning, and welcome to our rolling coverage of business, the financial markets and the world economy.

High interest rates are putting a growing strain on UK house prices, household wealth and company finances, new data today shows.

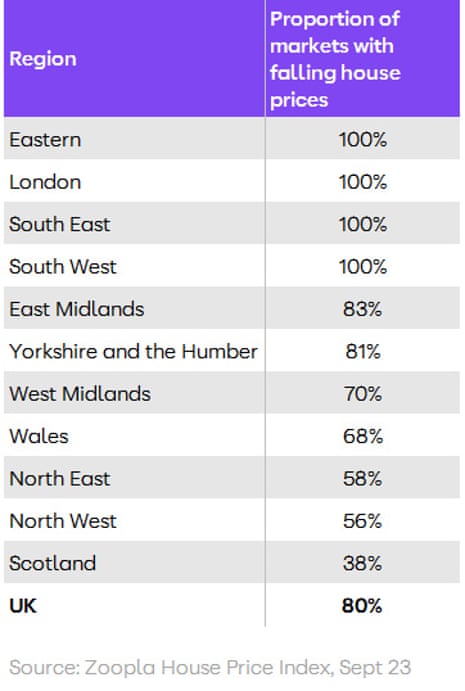

House prices are now falling in most parts of the UK, as high mortgage costs restrict how much buyers are willing, or able, to pay, according to data from property portal Zoopla this morning.

High borrowing costs are also pushing some firms into issuing profit warnings, a report from EY-Parthenon today shows (see here for more).

And the surge in interest rates to 5.25%, from 0.1% in late 2021, have triggered a sharp reversal in wealth levels across all parts of the UK, Resolution Foundation says today (see this post for more details).

Zoopla’s latest house price index show that prices have fallen over the last year in four in five local housing markets in the UK, with the largest declines in southern England towns such as Colchester (-3.5%), Canterbury (-3.4%) and Luton (-3.3%).

This is a sharp increase on six months ago, when one in 20 housing markets were showing annual falls.

Zoopla’s report shows average UK house prices are down 1.1% over the last year, which it says is the “most dramatic slowdown in price growth since 2009.”

It’s a smaller fall than Nationwide and Halifax have reported, though, based on their mortgage approvals data.

Zoopla points out, though, that the rise of the cash buyer continues. This group will account for one in three sales in 2023 as high mortgage rates hit buyer demand

Richard Donnell, executive director at Zoopla, says:

“House prices have proven more resilient than many expected over the last year in response to higher mortgage rates. However, almost a quarter fewer people will move home due to greater uncertainty and less buying power.

“Modest house price falls over 2023 mean it’s going to take longer for housing affordability to reset to a level where more people start to move home again. Income growth is finally increasing faster than inflation but mortgage rates remain stuck around 5% or higher. We believe that house prices will post further small falls, averaging 2%, over 2024 with 1m home moves.

“Slow house price growth and rising incomes over the next 12-18 months will improve affordability to levels last seen a decade ago, creating the potential for a rebound in home moves as consumer confidence returns.”

Also coming up today

Germany’s economy will be in the spotlight today, when the latest growth and inflation data is released. Economists predict German GDP fell by 0.3% in the last quarter, while inflation is seen cooling to 4%.

The agenda

9am BST: German Q3 GDP report

9.30am BST: UK mortgage lending and mortgage approvals for September

1pm BST: German inflation report for October

2.30pm BST: Dallas Fed Manufacturing Index

Filters BETA

Global bank HSBC has confirmed that the profit boost from higher interest rates has faded somewhat.

HSBC reported this morning that its net interest margin (NIM) dropped by two basis points in the last quarter to 1.7%.

NIM accounts for the difference in interest paid by borrowers and paid out to savers. It swelled as interest rates were raised over the last year, as banks were quicker to raise rates for borrowers than savers.

But this is now reversing, as customers move their money to “term products”, to lock in higher interest rates.

HSBC had a strong last quarter, though – it’s pre-tax profits more than doubled year-on-year to $7.7bn, which it says reflects “the positive impact of a higher interest rate environment”.

Here’s Victoria Scholar, head of investment at interactive investor, on Zoopla’s house price report:

Higher mortgage rates and the cost-of-living crisis have weakened buyer demand, which is languishing 25% below the five-year average in October. Transactions are being taken up by an increasing proportion of cash buyers up from 1 in 5 to 1 in 3 over the last five years. Many buyers are in wait-and-see mode, holding off for now, hoping that house prices will fall further, and mortgage rates will ease next year.

However strong wage growth, low unemployment and strict affordability testing rules have prevented an even steeper slide in house prices. Plus, there is a shortage of housing supply in the UK that is also stemming a more aggressive downturn in property prices.

Individuals and families are faced with the difficult choice between expensive rents and high mortgage rates with Zoopla estimating that for first-time buyers’ mortgage repayments are cheaper than rental costs even at 5.5% borrowing rates.”

Zoopla predicts that house prices will continue to drop next year, even if mortgage rates ease a little.

They say:

Assuming mortgage rates drop to 4.5% by the end of 2024, Zoopla expects that house price growth will remain negative with prices down 2% next year.

A faster fall in mortgage rates towards 4% would boost sales activity rather than house prices.

Concerns over the health of the UK economy may encourage the Bank of England not to raise interest rates higher.

The BoE will set borrowing costs on Thursday, and is expected to leave its base rate at 5.25%.

No-change is seen as a 95% chance by the money markets, with just a 5% chance of a hike to 5.5%.

The proportion of businesses who are blaming profit warnings on tighter credit conditions has risen to the highest level since the financial crisis.

A third of the profit warnings issued by UK companies in the last quarter blamed tougher credit conditions as a factor, the latest data from EY-Parthenon shows.

That’s the highest since 2008, and a clear sign that high interest rates are hitting the economy.

One-in-five profit warnings in the last quarter cited the slowing housing market.

Their latest quarterly survey of profit warnings also found that wider economic uncertainty is hitting companies, causing contracts to be delayed or cancelled and hitting consumer confidence.

In the last 12 months, 17.8% of UK-listed companies have issued a profit warning.

But almost half of firms in the FTSE Household Goods & Home Construction sector have issued warnings in the last year – which is the highest level of warnings across a 12-month period since 2008.

Amanda Blackhall O’Sullivan, EY-Parthenon Partner and Special Situations Advisory Leader, explains:

“Small and medium-sized housebuilders are feeling the effect of mortgage rate disruption and rising interest rates on demand and prices, which is resulting in tighter margins. However, there isn’t the same level of price or land value shock as we saw during the global financial crisis in 2008 and today’s sector is in a stronger position to weather the storm. The largest housebuilders have relatively low exposure to the slowing market and will have lower operational leverage and stronger balance sheets in comparison to 2008.

“On the other hand, construction contractors and material suppliers typically operate on higher costs and tighter margins, so may face a tougher period ahead. Earlier this year we saw smaller construction companies feeling the brunt of unprecedented cost, labour and supply chain stresses, and these will be exacerbated by a slowing market. As projects take longer to develop, we’re seeing stress move up the value chain and larger suppliers and sub-contractors are feeling the pressure.”

The recent rise in interest rates has been blamed for ending Britain’s wealth boom and causing total household wealth to plunge by a quarter since the Covid-19 pandemic.

A report by the Resolution Foundation, a thinktank, and Abrdn, the asset manager, said the fall was due to a drop in house prices and pension pots, which account for about £4 out of every £5 of total wealth, and played a leading role in rising wealth across the country over the 40 years leading up to the pandemic.

However, both have fallen in value since the Bank of England started raising interest rates in December 2021. While total household wealth was worth 840% of gross domestic product (GDP) in 2021, it had tumbled to 630% of GDP this year.

However, the split impact has not fallen evenly across the economy.

As a proportion of total household wealth Scotland, Wales and the north of England have seen the biggest drops of about 25%.

Resolution explains:

This reflects the larger proportion of wealth in these areas held in pensions, whose underlying assets have been hit hardest by rising interest rates. Meanwhile in the south and east of England, relatively resilient house prices have limited the wealth shock there so far. This could change as house prices come to reflect persistently higher mortgage rates.

Good morning, and welcome to our rolling coverage of business, the financial markets and the world economy.

High interest rates are putting a growing strain on UK house prices, household wealth and company finances, new data today shows.

House prices are now falling in most parts of the UK, as high mortgage costs restrict how much buyers are willing, or able, to pay, according to data from property portal Zoopla this morning.

High borrowing costs are also pushing some firms into issuing profit warnings, a report from EY-Parthenon today shows (see here for more).

And the surge in interest rates to 5.25%, from 0.1% in late 2021, have triggered a sharp reversal in wealth levels across all parts of the UK, Resolution Foundation says today (see this post for more details).

Zoopla’s latest house price index show that prices have fallen over the last year in four in five local housing markets in the UK, with the largest declines in southern England towns such as Colchester (-3.5%), Canterbury (-3.4%) and Luton (-3.3%).

This is a sharp increase on six months ago, when one in 20 housing markets were showing annual falls.

Zoopla’s report shows average UK house prices are down 1.1% over the last year, which it says is the “most dramatic slowdown in price growth since 2009.”

It’s a smaller fall than Nationwide and Halifax have reported, though, based on their mortgage approvals data.

Zoopla points out, though, that the rise of the cash buyer continues. This group will account for one in three sales in 2023 as high mortgage rates hit buyer demand

Richard Donnell, executive director at Zoopla, says:

“House prices have proven more resilient than many expected over the last year in response to higher mortgage rates. However, almost a quarter fewer people will move home due to greater uncertainty and less buying power.

“Modest house price falls over 2023 mean it’s going to take longer for housing affordability to reset to a level where more people start to move home again. Income growth is finally increasing faster than inflation but mortgage rates remain stuck around 5% or higher. We believe that house prices will post further small falls, averaging 2%, over 2024 with 1m home moves.

“Slow house price growth and rising incomes over the next 12-18 months will improve affordability to levels last seen a decade ago, creating the potential for a rebound in home moves as consumer confidence returns.”

Also coming up today

Germany’s economy will be in the spotlight today, when the latest growth and inflation data is released. Economists predict German GDP fell by 0.3% in the last quarter, while inflation is seen cooling to 4%.

The agenda

9am BST: German Q3 GDP report

9.30am BST: UK mortgage lending and mortgage approvals for September

1pm BST: German inflation report for October

2.30pm BST: Dallas Fed Manufacturing Index

https://news.google.com/rss/articles/CBMiqwFodHRwczovL3d3dy50aGVndWFyZGlhbi5jb20vYnVzaW5lc3MvbGl2ZS8yMDIzL29jdC8zMC9oaWdoLWludGVyZXN0LXJhdGVzLXVrLWhvdXNlLXByaWNlcy1ob3VzZWhvbGQtd2VhbHRoLWNvbXBhbnktZmluYW5jZXMtbW9ydGdhZ2UtYXBwcm92YWxzLWdlcm1hbi1lY29ub215LWJ1c2luZXNzLWxpdmXSAasBaHR0cHM6Ly9hbXAudGhlZ3VhcmRpYW4uY29tL2J1c2luZXNzL2xpdmUvMjAyMy9vY3QvMzAvaGlnaC1pbnRlcmVzdC1yYXRlcy11ay1ob3VzZS1wcmljZXMtaG91c2Vob2xkLXdlYWx0aC1jb21wYW55LWZpbmFuY2VzLW1vcnRnYWdlLWFwcHJvdmFscy1nZXJtYW4tZWNvbm9teS1idXNpbmVzcy1saXZl?oc=5

2023-10-30 08:03:00Z

2576802408

Tidak ada komentar:

Posting Komentar