LONDON, March 31 (Reuters) - British house prices slid in March at the fastest annual rate since the financial crisis, mortgage lender Nationwide said on Friday.

House prices fell 3.1% year-on-year, the biggest such drop since July 2009, Nationwide said. Compared with February this year, prices were 0.8% lower.

Economists polled by Reuters had expected prices to fall by 2.2% from a year earlier and by 0.3% in monthly terms.

Nationwide said the market was still feeling the effects of a "turning point" last year - the September economic agenda of former prime minister Liz Truss, which prompted a confidence crisis in British assets and hammered the mortgage market.

"It will be hard for the market to regain much momentum in the near term since consumer confidence remains weak and household budgets remain under pressure from high inflation," said Nationwide chief economist Robert Gardner.

Other gauges of the housing market have also looked subdued, although the Royal Institution of Chartered Surveyors this month said a slump in new buyer enquiries eased off a little.

A recession is generally defined in the UK as two consecutive quarters of declining GDP, and the economy had already contracted 0.2% in the third quarter.

Darren Morgan, director of economic statistics at the Office for National Statistics, said: "The economy performed a little more strongly in the latter half of last year than previously estimated, with later data showing telecommunications, construction and manufacturing all faring better than initially thought in the latest quarter.

"Households saved more in the last quarter, with their finances boosted by the government's energy bill support scheme.

"Meanwhile, the UK's balance of payments deficit with the rest of the world narrowed, driven by increased foreign earnings by UK companies, particularly in the energy sector."

The dominant services sector grew by 0.1%, boosted by a jump in nearly 11% for travel agents.

Manufacturing was up by 0.5%, driven by the pharmaceutical sector, and construction grew 1.3%.

'We still think the economy will slip into a recession this year'

Advertisement

The cost of living crisis has taken a heavy toll on consumer spending in recent months, with inflation remaining in double digits.

Updated predictions last week from the Bank of England, which had forecast that the economy entered recession in the second half of last year, ruled out the likelihood of a recession in 2023.

Ruth Gregory at Capital Economics said the upward revisions to the GDP figures for the third and fourth quarters showed that high inflation took a slightly smaller toll on the economy than previously thought.

"But with around two-thirds of the drag on real activity from higher rates yet to be felt, we still think the economy will slip into a recession this year," she said.

'Underlying resilience'

Chancellor Jeremy Hunt told reporters that the revised GDP figure showed there is "underlying resilience" in the UK economy.

Mr Hunt acknowledged, however, that many people across the country are "facing real pressure", with inflation remaining above 10%.

He said: "That's why we will continue to take the difficult decisions necessary to bring down inflation caused by what's happened in Ukraine.

"That is the way we will get back to healthy growth and relieve the pressure on families."

House prices have suffered their largest decline in 14 years as surging interest rates increased the cost of borrowing, according to Nationwide.

Property values were 3.1pc lower in March than they were a year ago, their sharpest decline since 2009.

House prices have fallen for a seventh month in a row and at a steeper rate than previous months.

Nationwide said prices were down 0.8pc in March, a bigger drop than 0.5pc in February and ahead of economists expectations of a 0.3pc fall.

Robert Gardner, the building society's chief economist, said: "It will be hard for the market to regain much momentum in the near term since consumer confidence remains weak and household budgets remain under pressure from high inflation.

"Housing affordability also remains stretched, where mortgage rates remain well above the lows prevailing at this point last year."

The UK’s new energy plan unveiled on Thursday is a missed opportunity full of “half-baked, half-hearted” policies that do not go far enough to power Britain’s climate goals, according to green business groups and academics.

The 1,000-page strategy has been criticised by many within Britain’s green sectors who fear the country could surrender its leading role in climate action because of the government’s “business as usual” approach to delivering green investments.

Environmental groups said the plans – which are expected to form the basis of the government’s revised strategy to meet its net zero ambitions– also risk falling short of meeting legally binding climate targets, which could trigger further court action.

Grant Shapps, the energy and net zero secretary, announced the wide-ranging strategy, which includes support for carbon capture projects, nuclear energy, offshore windfarms, electric vehicles, home heat pumps and hydrogen power.

However, most of the plans are based on existing government commitments and lack new funding.

Josh Burke, a senior policy fellow at the London School of Economics’ Grantham Research Institute, said the lack of a long-term, economy-wide investment plan “undermines investor confidence and prevents the UK from leading the green race”.

Joe Biden announced a $370bn green plan for the US last autumn to lower energy costs while accelerating private investment in clean energy solutions as part of his Inflation Reduction Act. Concerns have been raised that the huge subsidies in the plan could lure the UK’s key green industries across the Atlantic.

“Instead of grasping this historic moment the government has been left trailing behind the Inflation Reduction Act and is currently failing to capitalise on the opportunities a green transition will provide. Companies are making investment decisions now and in six months’ time the UK will be even further behind,” Burke said.

He argued that while the government was right to prioritise investment, the focus should be on technologies such as onshore wind that will reduce emissions in the short term and ensure energy security.

Ana Musat, an executive director at RenewableUK, which represents onshore wind developers, said the plans did “not go far enough to attract the investment we need in the renewable energy sector” amid “global competition for investment in renewable energy projects [which] is fiercer than ever”.

“We need much more than a ‘business as usual’ approach to kickstart investment on the level we need to boost energy security, cut consumer bills and reach net zero,” Musat said. “Without that, we won’t land the UK-wide economic benefits of building up new clean energy supply chains, as they will go elsewhere where the investment environment is more conducive and attractive.”

Ministers are also expected by the end of the week to publish a revised plan to reduce the UK’s carbon emissions to net zero by 2050, after a successful legal challenge by Friends of the Earth, ClientEarth and Good Law Project against the original plan.

Mike Childs, Friends of the Earth’s head of policy, said the groups lawyers were poised to act if the revised plan fell short. He warned that the government should be scaling up and accelerating the race to net zero, but the latest plans looked “half-baked, half-hearted and dangerously lacking ambition”.

“These announcements will do little to boost energy security, lower bills or put us on track to meet climate goals,” he said.

Mark Maslin, a professor of climatology at University College London, said: “At the moment the government announcement is more of the same, lacks insight to the energy issues and invests money in dead-end technology such as hydrogen.

“Yet again the UK government has missed the opportunity to radically change the UK energy production and market. This is the time that innovative business-led initiatives are needed.”

Drax's plans for a £2bn biomass carbon capture project in the UK have been rejected by the Government, but the power producer insists the project is still alive.

The company's shares were sent tumbling as much as 12pc after it failed to get so-called Track-1 status from the Department for Energy Security & Net Zero, which would have granted subsidies for its biomass project with carbon capture and storage.

However, Drax said it has been invited to enter "formal bilateral discussions" with the Government immediately.

The Government has also committed to publish its biomass strategy by the end of June, which will set out how the technology could be deployed.

Drax had said it was prepared to invest £2bn to fit the technology to some of the units at its Selby plant in North Yorkshire, supporting as many as 10,000 jobs.

Fears were raised in Whitehall this month that Drax may divert its £2bn of planned investment in carbon capture to the US after Joe Biden's massive package of green subsidies.

The President's Inflation Reduction Act offers subsidies and tax credits worth about $370bn (£309bn) for a range of green technologies.

More than 1,000 artificial intelligence experts, researchers and backers have joined a call for an immediate pause on the creation of “giant” AIs for at least six months, so the capabilities and dangers of systems such as GPT-4 can be properly studied and mitigated.

The demand is made in an open letter signed by major AI players including: Elon Musk, who co-founded OpenAI, the research lab responsible for ChatGPT and GPT-4; Emad Mostaque, who founded London-based Stability AI; and Steve Wozniak, the co-founder of Apple.

Its signatories also include engineers from Amazon, DeepMind, Google, Meta and Microsoft, as well as academics including the cognitive scientist Gary Marcus.

“Recent months have seen AI labs locked in an out-of-control race to develop and deploy ever more powerful digital minds that no one – not even their creators – can understand, predict, or reliably control,” the letter says.

“Powerful AI systems should be developed only once we are confident that their effects will be positive and their risks will be manageable.”

The authors, coordinated by the “longtermist” thinktank the Future of Life Institute, cite OpenAI’s own co-founder Sam Altman in justifying their calls.

In a post from February, Altman wrote: “At some point, it may be important to get independent review before starting to train future systems, and for the most advanced efforts to agree to limit the rate of growth of compute used for creating new models.”

The letter continued: “We agree. That point is now.”

If researchers will not voluntarily pause their work on AI models more powerful than GPT-4, the letter’s benchmark for “giant” models, then “governments should step in”, the authors say.

“This does not mean a pause on AI development in general, merely a stepping back from the dangerous race to ever-larger unpredictable black-box models with emergent capabilities,” they add.

Since the release of GPT-4, OpenAI has been adding capabilities to the AI system with “plugins”, giving it the ability to look up data on the open web, plan holidays, and even order groceries. But the company has to deal with “capability overhang”: the issue that its own systems are more powerful than it knows at release.

As researchers experiment with GPT-4 over the coming weeks and months, they are likely to uncover new ways of “prompting” the system that improve its ability to solve difficult problems.

One recent discovery was that the AI is noticeably more accurate at answering questions if it is first told to do so “in the style of a knowledgable expert”.

The call for strict regulation stands in stark contrast to the UK government’s flagship AI regulation white paper, published on Wednesday, which contains no new powers at all.

Instead, the government says, the focus is on coordinating existing regulators such as the Competition and Markets Authority and Health and Safety Executive, offering five “principles” through which they should think about AI.

“Our new approach is based on strong principles so that people can trust businesses to unleash this technology of tomorrow,” said the science, innovation and technology secretary, Michelle Donelan.

The Ada Lovelace Institute was among those that criticised the announcement. “The UK’s approach has significant gaps, which could leave harms unaddressed, and is underpowered relative to the urgency and scale of the challenge,” said Michael Birtwistle, who leads data and AI law and policy at the research institute.

“The government’s timeline of a year or more for implementation will leave risks unaddressed just as AI systems are being integrated at pace into our daily lives, from search engines to office suite software.”

Labour joined the criticism, with the shadow culture secretary, Lucy Powell, accusing the government of “letting down their side of the bargain”.

She said: “This regulation will take months, if not years, to come into effect. Meanwhile, ChatGPT, Google’s Bard and many others are making AI a regular part of our everyday lives.

“The government risks re-enforcing gaps in our existing regulatory system, and making the system hugely complex for businesses and citizens to navigate, at the same time as they’re weakening those foundations through their upcoming data bill.”

Mortgage lending in the UK fell sharply last month to the lowest level since the summer of 2021 – and was the lowest since 2016 if the Covid period is excluded – while mortgage approvals rose for the first time since August.

The latest Bank of England figures out this morning show that net mortgage lending to individuals fell from £2bn in January to £700m in February, the lowest since July 2021. Excluding the Covid pandemic, this is the lowest level of net borrowing since April 2016 when it was also £700m.

Mortgage approvals for house purchases increased to 43,500 in February, from 39,600 in January. This marked the first monthly increase since August 2022.

The ‘effective,’ or actual interest rate paid on newly drawn mortgages increased by 36 basis points, to 4.24% in February.

The data also showed consumers borrowed an additional £1.4bn in consumer credit in February, on a net basis, compared with £1.7bn borrowed during January. This was split between £600m of borrowing on credit cards and £800m of borrowing through other forms of consumer credit such as personal loans.

Filters BETA

More on UBS’s decision to bring back Sergio Ermotti as chief executive, a surprise move.

Ermotti, a former Merrill Lynch equity derivatives trader who led UBS for nine years until 2020 and slashed 10,000 jobs from the bank in 2012, faces the tough task of combining UBS and Credit Suisse, laying off staff, scaling back Credit Suisse’s investment bank and restoring confidence – in particular the wealthy who deposit their cash with UBS.

UBS chairman Colm Kelleher said about the decision to replace Ralph Hamers as CEO:

We felt we had a better horse.

He downplayed the importance of Ermotti’s nationality in getting the job:

This is not a Swiss solution.

Being Swiss helps. But the majority of our business is global.

Ermotti, 62, will leave the global reinsurance group Swiss RE, where he is chairman, to take the helm at UBS next Wednesday after what he described as a “call of duty”. He made a please for “a little bit of patience” over “a couple of months” to allow the bank to come up with a proper plan. He told a press conference:

We cannot rush into decisions which are regrettable.

UBS shares climbed 2% in early trading, and are now trading 1.6% higher at 18.02 Swiss francs.

Financial Times journalist Sam Gad Jones tweeted from Zurich:

The Bank of England has said that Britain’s banking system is not at risk from the kind of turmoil that has engulfed some regional banks in the US and Switzerland’s second-biggest lender Credit Suisse, which is being taken over by UBS.

However, the central bank’s financial policy committee (FPC) told regulators to move fast to toughen rules for funds used by Britain’s pension industry, which nearly collapsed last year after the former prime minister Liz Truss’s disastrous mini-budget.

But Britain’s broader banking sector is well-capitalised and has large liquid asset buffers, and would be able to continue lending to businesses if interest rates rise further and the economy worsens, the FPC said after its 23 March meeting.

Recent weeks have seen several overseas banks fail or come under severe stress. Banks’ share prices fell across the world and investors became more cautious.

The FPC is monitoring these events and the potential impact on UK banks and financial stability. UK banks are resilient and are strong enough to support households and businesses.

The FPC will continue to monitor developments closely, in particular for the risk that indirect spillovers impact the wider UK financial system.

The FPC told pension regulators to act “as soon as possible” to limit the risks posed by liability-driven investment (LDI) funds.

The central bank was forced to step in with a new round of government bond purchases last autumn after Truss’s package of unfunded tax cuts triggered a surge in gilt yields.

LDI funds should set aside enough liquidity to ensure they can cope with a jump in government bond yields of at least 250 basis points, on top of other protections against wild market swings, the Bank said today.

The sharp decline in UK mortgage lending to just £700m in February suggests house prices have further to fall, said Thomas Pugh, economist at the tax and consulting firm RSM UK.

Admittedly, a small rise in mortgage approvals, the first since August, suggests that demand may have already reached its nadir. But higher interest rates and falling real incomes will limit buyers’ ability to meet high prices. We expect a peak to trough fall in house prices of between 5% and 10%.

Meanwhile, the sharp drop in lending to the private sector suggests that banks were already curtailing lending, even before the latest issues in the financial sector. We estimate that the tightening in financial conditions around the recent turmoil is equivalent to a 25bps increase in interest rates.

There was also little sign that the recent upticks in consumer confidence have led to households borrowing more or saving less. Indeed, consumer credit growth was slightly lower in February than in January. What’s more, consumer savings rose from £3.3bn in January to £3.6bn in February. And it seems that those households with savings are moving them to longer term accounts that pay more interest, rather than spending them. Net flows into time deposits remained strong at £6.8 billion in February, but this was largely offset by net flows of interest-bearing sight deposits at -£6.1 billion in February.

We are yet to see most of the impact of the huge rise in interest rates over the last year and real incomes are likely to drop further in the first half of 2023. Even if the UK does avoid a technical recession of two consecutive quarters of negative GDP growth, we will still enter a ‘slowcession’, where growth essentially flatlines. It will probably be the end of 2024 before the UK economy is back to its pre-pandemic size, representing four years of stagnation.

Jeremy Hunt is being quizzed by MPs on the Commons Treasury committee about the spring budget.

He said the Treasury has not yet decided how much funding the Department of Health and Social Care will get to fund a pay deal for NHS workers.

He explained that government departments normally fund pay settlements from the money they get in the spending review. But in exceptional circumstances they can speak to the Treasury about extra help.

He said this is a special situation because of high inflation. There will be a discussion about how much help health will get, but this hasn’t happened yet.

You can read more on our politics live blog with Andy Sparrow:

Samuel Tombs, chief UK economist at Pantheon Macroeconomics, has also looked at the data.

The continued weakness of house purchase mortgage approvals in February confirms that buyers are waiting for affordability to improve, either via a large correction in house prices or a larger fall in mortgage rates than seen to date, before re-entering the market.

Households showed further signs in February of drawing on the savings they accumulated during the pandemic to sustain their consumption.

Ashley Webb, UK economist at Capital Economics, said:

February’s money and credit data release suggests that higher interest rates were a further drag on lending in February, particularly in the housing market. That’s before the recent concerns over the health of global banks, which may prompt UK banks to tighten credit conditions further. Our hunch is that the economy will still enter a recession later this year.

Mortgage approvals rose for the first time in six months from 39,600 in January to 43,500 in February. But that still leaves them languishing around 35% below pre-pandemic levels. And the monthly increase in net mortgage lending eased from £2bn to £700m… And with interest rates likely to stay high for all this year, housing market activity will likely remain weak for some time yet.

But higher interest rates still appear to be less effective elsewhere in the economy so far. The 1.2% month-on-month surge in retail sales volumes in February suggests households continued to spend in February. And today’s data release suggests households partly financed that spending by increasing borrowing.

Overall, it’s clear that higher interest rates are weighing on the housing market. But they appear to be having less of a drag in other areas of the economy as households continue to borrow to support spending. However, the recent tightening in financial conditions might cause banks to restrict their credit supply, which would amplify the drag on real activity, or at least bring it forward.

Mortgage lending in the UK fell sharply last month to the lowest level since the summer of 2021 – and was the lowest since 2016 if the Covid period is excluded – while mortgage approvals rose for the first time since August.

The latest Bank of England figures out this morning show that net mortgage lending to individuals fell from £2bn in January to £700m in February, the lowest since July 2021. Excluding the Covid pandemic, this is the lowest level of net borrowing since April 2016 when it was also £700m.

Mortgage approvals for house purchases increased to 43,500 in February, from 39,600 in January. This marked the first monthly increase since August 2022.

The ‘effective,’ or actual interest rate paid on newly drawn mortgages increased by 36 basis points, to 4.24% in February.

The data also showed consumers borrowed an additional £1.4bn in consumer credit in February, on a net basis, compared with £1.7bn borrowed during January. This was split between £600m of borrowing on credit cards and £800m of borrowing through other forms of consumer credit such as personal loans.

Flora Bocahut, equity analyst at Jefferies, has sent us her thoughts on the new UBS boss.

Sergio Ermotti is well-known, having been UBS CEO for nine years and restructured the bank.

Ermotti is well-known and, in our view, benefits from a strong & adequate track record for the upcoming (challenging) task of restructuring & integrating Credit Suisse, having been previously UBS CEO for 9 years and having already tackled the restructuring of the bank, redefined the strategy, downsized the investment bank and refocused the capital allocation towards wealth management.

Ermotti, a Swiss national, was appointed CEO of UBS in 2011, having previously worked at Merrill Lynch for 16 years (from 1987 to 2004), holding various positions esp. in equity derivatives up to becoming Co-Head of Global Equity Markets and a member of the Executive Management Committee for Global Markets & Investment Banking at Merrill Lynch in 2001.

In 2005, he joined Unicredit, initially as Head of Markets & IB, up until becoming Deputy CEO in charge of CIB & Private Banking in 2007 (to 2010). He joined UBS in 2011, initially as CEO for EMEA, then as interim & permanent Group CEO later that same year. He left UBS in 2020 to join Swiss Re (where he is currently the Chairman of the Board), succeeded as UBS Group CEO by Ralph Hamers (who was previously the CEO of ING Group).

Here is our full story on Next.

Next said it expected to raise prices more slowly in the coming year in a sign of easing inflation, as the clothing and homeware retailer reported record annual profits of £870m.

The FTSE 100 company increased profits by 5.7% in the year to 31 January, while total sales from trading rose by 8.4% compared with the previous year to £5.1bn, it said on Wednesday.

However, Next warned of a “very challenging” 2023 as its shoppers struggle with the cost-of-living crisis, with sales forecast to fall by 1.5% this year, while profits will also drop back. Its shares fell 5.7% on the news.

Retailers and consumers have been struggling with surging prices triggered by the recovery from the coronavirus pandemic and the Russian invasion of Ukraine.

European stocks have made modest gains, as the major bourses continue to drift higher following last week’s turmoil.

The FTSE 100 has ticked up 0.6% to 7,527, its highest level since last Thursday. We’re seeing similar upwards drifts for the Dax and CAC, too, as investors put banking stresses behind them.

US futures are up, pointing to a higher open on Wall Street later.

Neil Wilson, chief market analyst at Markets.com, said about UBS’s decision to bring back ex-boss Sergio Ermotti to take the reins once more:

It’s like calling back Fergie to manage Scotland. Ok it’s not, but I figured we need some analogy that references Scotland + football after last night’s heroics from Steve Clarke’s men.

UBS shares rallied 2% to above 18 Swiss francs in early trade as the bank named ex-boss Sergio Ermotti as new CEO, taking over from Ralph Hamers on 5 April.

Investors seem to be saying they like the prospect of the old hand on the tiller. UBS faces no small challenge in digesting Credit Suisse. Hamers can’t feel too good about being strong-armed into buying a mare and then not even getting to ride her.

The perception – rightly or wrongly – will be that Hamers was not considered right to lead the new behemoth through what’s going to be a tricky period of consolidation, integration and, no doubt, litigation.

Bupa Dental Care is to cut 85 dental practices this year in a move that will affect 1,200 staff across the UK, amid a national shortage of dentists and “systemic” challenges across the industry.

The private healthcare group said patients at the affected practices had not been able to access the NHS dental service they need.

The provider, which provides private and NHS dental care, has not been able to recruit enough dentists for NHS care in many practices for months and in some cases years, it said.

Bupa said the 85 practices will be closed, sold or merged later this year, bringing the total number of practices in the UK down to 365. All the practices will remain open as usual in the meantime.

The boss of the fashion and homewares retailer Next said he does not think the downturn in the UK economy will be long lasting.

Lord Simon Wolfson told Reuters:

We’ve never thought that the downturn would be long-lasting.

Yesterday, Next bought the Cath Kidston brand name for £8.5m, after the vintage-inspired British retailer fell into administration for the second time in two years.

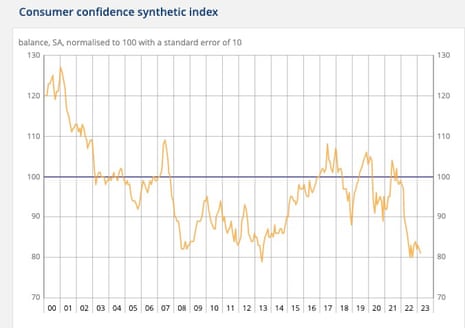

In France, household confidence slipped slightly in March.

According to the economics institute Insee (Institut national de la statistique et des études économiques), its monthly indicator dropped one point to 81 in March and remained well below its long-term average of 100 between 1987 and 2022.

Households’ balances of opinion on their future and past financial situation are stable, as is the one on major purchases intentions, all three remain well below their long-term average.

The share of households considering it is a good idea to save has fallen again after a sharp increase in February. The balance of opinion has declined four points but remains well above its long-term average.

In Germany, consumer confidence continues to improve as energy prices ease, although a full recovery is still some way off.

The GfK institute’s closely watched index recorded an unexpected rise to -29.5 going into April, from a revised reading of -30.6 in March. Markets had expected a drop to -33.1.

April’s rise is the sixth monthly improvement in a row, but the pace has slowed noticeably compared with previous months.

GfK consumer expert Rolf Buerkl said:

The anticipated loss of purchasing power is preventing a sustained recovery of domestic demand.

This is also indicated by the still very low level of consumer confidence.

The income outlook is currently benefiting from noticeably lower prices for energy, especially for gasoline and heating oil. Nevertheless, inflation will remain high.

The subindex measuring income expectations was the main contributor to the increase in sentiment, rising to its highest level in 10 months.

European stocks have opened slightly higher, the third day of gains.

The UK’s FTSE 100 index is up 21 points, or 0.3%, to 7,506, while Germany’s Dax and France’s CAC rose 0.7%, and Spain’s Ibex and Italy’s FTSE MiB advanced 05%.

The pound has slid 0.2% against the dollar to $1.2313.

Victoria Scholar, head of investment at the trading platform interactive investor said:

Ermotti previously served as chief executive of UBS from 2011 until 2020 and is currently the chairman of Swiss Re. Ralph Hamers who has been in the top job since November 2020 is stepping down ‘in light of the new challenges and priorities facing UBS’. Ermotti said ‘the task at hand is an urgent and challenging one’.

Having steered UBS through the aftermath of the 2008 global financial crisis and a rogue-trading scandal, Ermotti is a dab hand at crisis management. He also helped UBS to navigate through the onset of the pandemic and the corresponding market volatility throughout most of 2020.

The new CEO will have the immediate challenges of cutting staff, reducing Credit Suisse’s investment bank, finding other synergies between the two lenders and convincing shareholders about the prospects of the combined entity.

Good morning, and welcome to our rolling coverage of business, the financial markets and the world economy.

Some calm has returned to stock markets and European markets notched up some modest gains yesterday but struggled for direction.

The UK high street chain Next has said it expects to raise its prices more slowly over the year ahead as it revealed better-than-expected annual profits of £870m.

Like-for-like price inflation in the spring and summer collections is expected to be +7% and, in the autumn/winter, +3%, down from +8% and +6% respectively.

We now believe price rises in the second half will be materially lower than we initially feared.

Next cited a significant reduction in the cost of container freight as shipping capacities return to normal, as well as improving factory gate prices (the price at which it purchases the goods in the country of origin). The majority of these benefits will be felt in the second half of the year.

In a surprise move, UBS has brought back its former boss Sergio Ermotti (who currently chairs the reinsurance group Swiss Re) and appointed him as chief executive, to steer its massive takeover of Credit Suisse.

He will replace the current CEO Ralph Hamers on 5 April. Hamers, who succeeded Ermotti in November 2020, will stay on as adviser during a transition period, Switzerland’s largest bank said in a statement.

Ermotti previously ran the bank for nine years and oversaw a restructuring of the investment bank. UBS said:

This unique experience, together with his deep understanding of the financial services industry in Switzerland and globally, make Sergio Ermotti ideally placed to pursue the integration of Credit Suisse.

The move comes less than two weeks after UBS agreed to take over Credit Suisse in a in a £2.65bn deal forced through by Swiss authorities who feared that a failure to protect depositors would trigger a global banking meltdown.

Here’s an old tweet from Tracy Alloway, co-host of Bloomberg’s Odd Lots podcast:

Ermotti said:

The task at hand is an urgent and challenging one.

In order to it in a sustainable and successful way, and in the interest of all stakeholders involved, we need to thoughtfully and systematically assess all options.

The task involves combining two banks with $1.6 trillion in assets, more than 120,000 staff and a complex balance sheet. Hamers has no big M&A experience.

Later this morning, we will get lending data from the Bank of England that will give an insight into the state of the UK housing market and consumer lending more generally.

Michael Hewson, chief market analyst at CMC Markets UK, said:

UK mortgage approvals have seen a sharp slowdown in the last few months as higher interest rates and the rising cost of living serves to crimp demand, even as the lead-up to Christmas tends to see a slowdown in demand.

In January mortgage demand fell to its lowest level since 2020 at 39.6k, and today’s February numbers aren’t expected to see a significant pickup with expectations of around 40k.

In January net consumer credit saw a sharp pickup to £1.6bn, after a slowdown at the end of last year that saw consumer borrowing slow to £800m from £1.5bn. This stop start nature of consumer borrowing points to a UK consumer that is very sensitive to the rising cost of living, and while consumer confidence has improved in recent months it remains very fragile.

Today’s consumer credit numbers for February are expected to show a modest slowdown to £1.2bn, with recent trends in retail sales showing that discretionary demand has started to pick up as energy prices have fallen back.

The Agenda

9.30am BST: Bank of England Mortgage approvals and consumer credit for February

9.45am BST: MPs on Treasury committee grill Jeremy Hunt on spring budget

10.30am BST: Bank of England Minutes of financial policy committee meeting

2pm BST: Swiss National Bank Quarterly bulletin

3pm BST: Federal Reserve vice-chair for supervision, Michael Barr, testifies on SVB collapse

A looming British ban on the sale of new petrol and diesel cars was thrown into chaos on Tuesday after Brussels watered down its own restrictions amid opposition from the German auto industry.

Experts and politicians warned that British rules due to take effect in 2030 are untenable following the European climbdown, which will allow internal combustion engines as long as they burn carbon-neutral petrol alternatives.

The European Union will now ban the sale of petrol and diesel cars from 2035 but permit these so-called e-fuels following a backroom compromise forced on it by the German authorities and signed off on Tuesday night.

Sources suggested that Whitehall was considering following the Commission's lead by also allowing an e-fuel exemption. British carmakers Aston Martin and McLaren are already understood to be examining e-fuels as an option for powering future models.

Critics of the Government's net zero plans seized on the European Union's decision as evidence that a total policy rethink is needed, while campaigners including Greenpeace have said that it could slow down electric vehicle adoption.

It comes as Grant Shapps, the Energy Secretary, prepares to announce new green measures as part of an “energy security day” on Thursday.

The former Tory leader Sir Iain Duncan Smith said: “The 2030 deadline for the elimination of petrol and diesel engine cars in the UK is simply not achievable.

“Unless we delay, we hand a massive boost to the Chinese car manufacturers. They are already dominant.”

Britain is to ban the sale of new cars that run on petrol and diesel only in seven years' time under plans drawn up by former prime minister Boris Johnson.

New hybrids will still be allowed until 2035, at which point the UK will only permit fully electric cars and other zero-emission vehicles, such as those which burn hydrogen.

The EU's e-fuel exemption will allow a synthetic alternative to petrol which is made by mixing carbon dioxide captured from the air with hydrogen obtained by splitting water molecules using renewable energy.

This is expected to be far more expensive than petrol, meaning it will initially benefit high-end carmakers whose customers will not be put off by the costs involved.

However, Benedetto Vigna, the boss of Ferrari, said this week that he expects the price to fall in coming years and experts believe it could be the thin end of a wedge that would allow carmakers to focus on producing lower-cost e-fuels instead of expensive battery powered cars.

Andrew Graves, a car industry veteran and professor at the University of Bath, said: “I think it's a very exciting technology that we're looking at, so that we can not only use it for things like motorsport, but we can also more importantly use it for keeping existing vehicles on the road.

“I think there's a lot of things that the Government needs to look at before it goes hell bent on just having a blanket ban on diesel or petrol.”

Mr Graves added that there is already a risk that not enough electric car chargers and battery-making plants will have been built when the ban takes effect – a problem that may worsen if carmakers sense it is being watered down.

Brussels' decision is also likely to raise questions about how enforceable a British ban on petrol and diesel would be if similar rules are not followed in the EU – particularly given the open border between Ireland and Northern Ireland, which could facilitate easy movement of new European vehicles.

It comes as Mr Shapps prepares to unveil ways to speed up Britain’s move towards nuclear energy, including the confirmation that the Government wants 25pc of UK electricity to be generated from nuclear by 2050.

He will also kick-start the use of small modular reactors in Britain, and improve the country’s capacity for carbon capture storage.

An announcement on the timetable for sales of new petrol and diesel cars is likely to form part of the package.

But the EU's actions will complicate the picture and embolden opponents.

The climbdown follows months of lobbying by the German government seeking an exemption for cars running on e-fuels

Credit: REUTERS/Matthias Rietschel/File Photo

Sir John Redwood, a former Tory cabinet minister, said: “Britain is in a desperate struggle to keep its car industry, and if we insist on phasing petrol and diesel out well before anyone else, we will find it harder to attract investment.

“The Government needs to listen to the Germans and take advice on this. The more permissive an economy is, and the fewer bans there are, the better to promote growth.”

Ben Houchen, the Tees Valley mayor, said: “It comes down to the fact of the importance of a transition. What the Europeans are realising, and what we will realise quite shortly is that a transition is quite important.

“And a transition can't be a cliff-edge in 2025 or 2030. It is going to take longer to transition. Not just the technology, but for businesses and the economy to accommodate the abolition of certain technologies.

“I don't think it compromises the push to net zero. It just helps people realise that the transition has a longer tail than people realise.”

The EU climbdown followed months of lobbying by the German government on behalf of its car manufacturing industry. Porsche has invested $75m (£61m) in a pilot plant to make e-fuels.

The Telegraph understands that the British government is prepared to follow the EU's lead, with the Department for Transport understood to be amenable towards synthetic fuels so long as the industry can prove that they will be carbon neutral.

A government spokesman said: “We remain committed to ensuring all new cars and vans are zero emission at the tailpipe by 2035, and have invested more than £2bn to help people switch.

“Today drivers on England’s motorways and major A roads are never more than 25 miles from a rapid chargepoint, and we expect the charging network to expand tenfold by 2030.”

Greg Smith, a Tory MP who sits on the transport select committee, said: "Groupthink has dictated battery electric to be the way forward for too long when we're already seeing the technology fail and not develop at the pace people need.

"The 2030 ambition isn't realistic in the first place and we need the innovators and the automotive companies to be given the time and space to produce a time and space and not just jump to the betamax that's available now."

Philip Davies, a member of the Tory net zero scrutiny group, said: “It's a devil when you're getting more common sense out of the EU than you are the UK Government. This arbitrary, ridiculous 2030 deadline is idiotic and everybody knows it's idiotic. Nobody seems to be able to say that the emperor's got no clothes on, even though everybody can see it.

"If a rare outbreak of common sense in the EU is what it takes for the Government to change their position, hallelujah to that."

In the UK, Bentley is understood to be pressing ahead with its programme of electrification, shunning the extra expense of developing new combustion cars.

However, sources at Aston Martin and McLaren said the companies are interested in e-fuels.

Greenpeace described the Brussels climbdown as a "rotten compromise".

Banks face greater regulation on the amount of money they must hold to cover potential bank runs in the wake of the collapse of Silicon Valley Bank, a Bank of England chief has warned.

Sam Woods, the chief executive of the Prudential Regulation Authority, the Bank's financial services regulatory body, said the speed of the withdrawals from the Californian lender had concerned policy makers.

He told MPs on the Treasury select committee that it created a "question for all of us" about whether current ratios of deposits banks are required to hold are high enough.

During the same evidence session, Bank of England Governor Andrew Bailey said the collapse was the fastest since Barings Bank in 1995.

Mr Woods, who is also deputy governor at the Bank of England, said regulators would look again at the liquidity coverage ratio, which requires banks to hold enough liquid assets to fund cash withdrawals for 30 days.

Mr Woods told MPs: "Where I think there might be more of a policy question - it's an international question in which we'll take a close interest - is around the calibration of the liquidity coverage ratio.

"That's the one-month liquidity that the banks have to hold.

"A very striking feature of this Silicon Valley Bank run - not so much of the Credit Suisse run - was the speed with which it took place.

"You can see $2.9bn of deposits going out in a day on Friday 9th March.

"The sort of outflow rates that we have - the percentage of deposits that are assumed to run out - in that liquidity coverage ratio.

"Some actually are 100pc. So deposits from financial institutions are assumed all to go but operational deposits are less than that and retail deposits less still.

"So I think there’s going to be a question for all of us as to whether those outflow rates are quite high enough."

William Hill has been fined a record £19m for “widespread and alarming” social responsibility and anti-money-laundering failures, the Gambling Commission has announced.

Three gambling businesses owned by William Hill will pay a total of £19.2m – the largest penalty in the commission’s history – for failing to protect customers, some of whom were allowed to spend thousands of pounds at a time without checks.

The regulator said it had considered suspending William Hill’s licence but this was avoided after the company worked rapidly to make changes.

Social responsibility failures at William Hill businesses included allowing one customer to open a new account and spend £23,000 in 20 minutes; allowing another to open an account and spend £18,000 in 24 hours; and allowing a third customer to spend £32,500 over two days – all without any checks. The commission said the company failed to carry out checks at an early stage in the customer’s journey, which meant one user lost £14,902 in 70 minutes.

William Hill was also found to have failed to identify risk of harm or intervene with certain customers earlier enough – one lost £54,252 in four weeks without the operator seeking income evidence or carrying out adequate checks. The firm also failed to apply a 24-hour delay between receiving a request for an increase in a credit limit and granting it: one customer was allowed to immediately place a £100,000 bet when his credit limit had been set at £70,000.

WHG (International) Ltd, which runs williamhill.com, will pay £12.5m; Mr Green Ltd, which runs mrgreen.com, will pay £3.7m; and William Hill Organisation Ltd, which operates 1,344 gambling premises across Britain, will pay £3m.

The Gambling Commission chief executive, Andrew Rhodes, said: “When we launched this investigation the failings we uncovered were so widespread and alarming serious consideration was given to licence suspension.

“However, because the operator immediately recognised their failings and worked with us to swiftly implement improvements, we instead opted for the largest enforcement payment in our history.”

Ineffective controls allowed 331 customers to gamble with WHG (International) Ltd despite having self-excluded from mrgreen.com.

Anti-money-laundering failures included allowing customers to deposit large amounts without conducting appropriate checks. One customer was able to spend and lose £70,134 in a month, while another lost £38,000 in five weeks and a third lost £36,000 in four days.

An 888 spokesperson said: “The settlement relates to the period when William Hill was under the previous ownership and management. After William Hill was acquired, the company quickly addressed the identified issues with the implementation of a rigorous action plan.

“The entire group shares the Gambling Commission’s commitment to improve compliance standards across the industry and we will continue to work collaboratively with the regulator and other stakeholders to achieve this.”

Since the start of 2022, the Gambling Commission has concluded 26 enforcement cases, which resulted in operators paying more than £76m because of regulatory failures.

Rhodes said: “In the last 15 months we have taken unprecedented action against gambling operators, but we are now starting to see signs of improvement. There are indications that the industry is doing more to make gambling safer and reducing the possibility of criminal funds entering their businesses.

“Operators are using algorithms to spot gambling harms or criminal risk more quickly, interacting with consumers sooner, and generally having more effective policies and procedures in place.”

/cloudfront-us-east-2.images.arcpublishing.com/reuters/RRFKMCJSFRJITDIYCHVKZQGNQI.jpg)